데이터 사이언스 07 시계열 데이터 01-statsmodels

- 1. 시계열 데이터 - using Numpy

- 2. StatsModels : 예제1 - 비행기 여객

- 3. statsmodels - 시계열 데이터(Time Series)

- 3. statsmodels : 예제2- 하와이 대기 CO2비중

1. 시계열 데이터 - using Numpy

- 시간 순서로 되어 있는 데이터를 표현하기

- 위 데이터를 방정식으로 표현하기

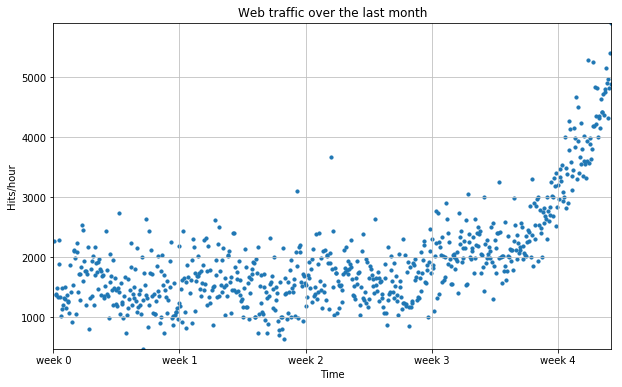

1) 예제 1 - 웹 트래픽 분석

- numpy에서 텍스트를 읽는 함수 :

numpy.genfromtxt - 탭(

\t)으로 구분되어 있다고 설정한다. -

원본 데이터(raw data)는 1열이 한 시간 단위, 2열이 웹페이지 hit이다.

- raw data(./data_science/web_traffic.tsv) 에서 시간축(1열)과 hit 수(2열)로 분리하기

import numpy as np

import matplotlib.pyplot as plt

%matplotlib inline

data = np.genfromtxt("./data_science/07. web_traffic.tsv")

data

array([[ 1.00000000e+00, 2.27200000e+03],

[ 2.00000000e+00, nan],

[ 3.00000000e+00, 1.38600000e+03],

...,

[ 7.41000000e+02, 5.39200000e+03],

[ 7.42000000e+02, 5.90600000e+03],

[ 7.43000000e+02, 4.88100000e+03]])

# 첫번째 열 [ : , 0 ]은 시간(x)

# 두번째 열 [ : , 1 ]은 hit수(y)

x = data[:, 0]

y = data[:, 1]

# 의미없는 데이터 확인

np.sum( np.isnan(y) )

8

# 사용가능한 데이터 얻기

x = x[~np.isnan(y)]

y = y[~np.isnan(y)]

2) 시각화

# 그래프

plt.figure( figsize=(10, 6) )

plt.scatter( x, y, s=10 )

plt.title("Web traffic over the last month")

plt.xlabel("Time")

plt.ylabel("Hits/hour")

plt.grid( True, linestyle='-', color='0.75' )

# 데이터가 가급적 화면에 꽉 차도록 autoscale을 적용함

plt.autoscale( tight=True )

# plt.xticks([A], [B]) ~ A라고 표기될 x축 라벨을 B로 표기

plt.xticks( [w*7*24 for w in range(5)] , [ 'week %i' % w for w in range(5) ] )

plt.show()

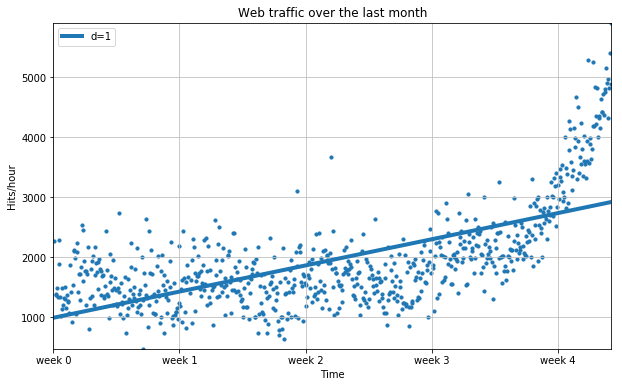

3) 에러 정의하기

- RMS

- 실제값( y )과 예측값( f(x) )의 차이( error )를 제곱하여 평균을 구한 후 root를 취한 값

- 1차 함수 f(x)를 구하기

def error(f, x, y):

return np.sqrt( np.mean( f(x) - y )**2 )

# 1차 함수에서 기울기와 y절편을 구한다.

np.polyfit( x, y, 1)

array([ 2.59619213, 989.02487106])

# 위 기울기와 y절편으로 1차 함수를 만들기

fp1 = np.polyfit( x, y, 1 )

f1 = np.poly1d( fp1 )

error(f1, x, y)

8.2163875098942091e-13

4) 1차 함수 그래프

fx = np.linspace( 0, x[-1], 1000 )

plt.figure( figsize=(10, 6) )

plt.scatter( x, y, s=10 )

# 1차 추쇄선 삽입

plt.plot( fx, f1(fx), lw=4 )

plt.title("Web traffic over the last month")

plt.xlabel("Time")

plt.ylabel("Hits/hour")

plt.grid( True, linestyle='-', color='0.75' )

# 데이터가 가급적 화면에 꽉 차도록 autoscale을 적용함

plt.autoscale( tight=True )

# plt.xticks([A], [B]) ~ A라고 표기될 x축 라벨을 B로 표기

plt.xticks( [w*7*24 for w in range(5)] , [ 'week %i' % w for w in range(5) ] )

plt.legend( [ "d=%i" % f1.order], loc=2 )

plt.show()

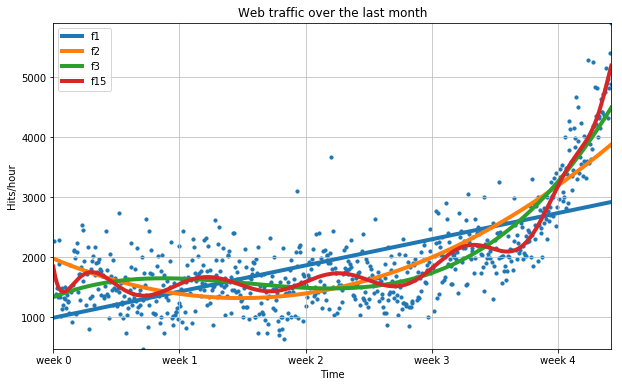

5) 2차 이상 함수 그래프

- 15차 함수에서 오히려 에러가 더 커진다.

f2p = np.polyfit(x, y, 2)

f2 = np.poly1d( f2p )

f3p = np.polyfit( x, y, 3 )

f3 = np.poly1d( f3p )

f15p = np.polyfit( x, y, 15 )

f15 = np.poly1d(f15p)

error( f1, x, y), error( f2, x, y), error(f3, x, y), error(f15, x, y)

(8.2163875098942091e-13,

3.7122232725425643e-13,

2.2149598859503965e-13,

3.7538309301094562e-05)

plt.figure( figsize=(10, 6) )

plt.scatter( x, y, s=10 )

# 추쇄선 삽입

plt.plot( fx, f1(fx), lw=4, label='f1')

plt.plot( fx, f2(fx), lw=4, label='f2')

plt.plot( fx, f3(fx), lw=4, label='f3')

plt.plot( fx, f15(fx), lw=4, label='f15')

plt.title("Web traffic over the last month")

plt.xlabel("Time")

plt.ylabel("Hits/hour")

plt.grid( True, linestyle='-', color='0.75' )

# 데이터가 가급적 화면에 꽉 차도록 autoscale을 적용함

plt.autoscale( tight=True )

# plt.xticks([A], [B]) ~ A라고 표기될 x축 라벨을 B로 표기

plt.xticks( [w*7*24 for w in range(5)] , [ 'week %i' % w for w in range(5) ] )

plt.legend( loc=2 )

plt.show()

2. StatsModels : 예제1 - 비행기 여객

1) 소개

- numpy 보다 통계치 표현에 더 유용한 도구를 사용하자.

- StatsModel : Python에서 통계 관련 함수와 모델링 기법을 제공하는 모듈이다.

2) 설치

➜ pip install -U statsmodels

Collecting statsmodels

Downloading statsmodels-0.8.0-cp36-cp36m-manylinux1_x86_64.whl (6.3MB)

100% |████████████████████████████████| 6.3MB 159kB/s

Requirement already up-to-date: pandas in /home/learn/.pyenv/versions/3.6.2/envs/Jupyter/lib/python3.6/site-packages (from statsmodels)

Requirement already up-to-date: scipy in /home/learn/.pyenv/versions/3.6.2/envs/Jupyter/lib/python3.6/site-packages (from statsmodels)

Collecting patsy (from statsmodels)

Downloading patsy-0.5.0-py2.py3-none-any.whl (232kB)

100% |████████████████████████████████| 235kB 1.7MB/s

Collecting numpy>=1.9.0 (from pandas->statsmodels)

Downloading numpy-1.14.0-cp36-cp36m-manylinux1_x86_64.whl (17.2MB)

100% |████████████████████████████████| 17.2MB 56kB/s

Requirement already up-to-date: python-dateutil>=2 in /home/learn/.pyenv/versions/3.6.2/envs/Jupyter/lib/python3.6/site-packages (from pandas->statsmodels)

Requirement already up-to-date: pytz>=2011k in /home/learn/.pyenv/versions/3.6.2/envs/Jupyter/lib/python3.6/site-packages (from pandas->statsmodels)

Requirement already up-to-date: six in /home/learn/.pyenv/versions/3.6.2/envs/Jupyter/lib/python3.6/site-packages (from patsy->statsmodels)

Installing collected packages: numpy, patsy, statsmodels

Found existing installation: numpy 1.13.3

Uninstalling numpy-1.13.3:

Successfully uninstalled numpy-1.13.3

Successfully installed numpy-1.14.0 patsy-0.5.0 statsmodels-0.8.0

3) 예제 데이터

statsmodels모듈이 제공하는 R용 데이터들- 위 모듈의 목표는 기존의 R 유저가 python에서 동일하게 분석할 수 있게 하는 것이다.

import warnings

warnings.filterwarnings("ignore")

import itertools

import pandas as pd

import numpy as np

import statsmodels.api as sm

import matplotlib.pyplot as plt

plt.style.use('fivethirtyeight')

%matplotlib inline

df = sm.datasets.get_rdataset("AirPassengers").data

df.head(3)

| time | AirPassengers | |

|---|---|---|

| 0 | 1949.000000 | 112 |

| 1 | 1949.083333 | 118 |

| 2 | 1949.166667 | 132 |

- time 부분에 소수표현이 있다. 이를 datetime형식으로 바꿔보자

def yearfraction2datetime( yearfraction, startyear=0 ):

import datetime, dateutil

year = int( yearfraction ) + startyear

month = int( round( 12*( yearfraction - year) ) )

delta = dateutil.relativedelta.relativedelta( months=month )

date = datetime.datetime( year, 1, 1) + delta

return date

yearfraction2datetime(1949.333333)

datetime.datetime(1949, 5, 1, 0, 0)

import datetime, dateutil

dateutil.relativedelta.relativedelta( months=15 )

relativedelta(years=+1, months=+3)

df["datetime"] = df.time.map( yearfraction2datetime )

df.tail(3)

| time | AirPassengers | datetime | |

|---|---|---|---|

| 141 | 1960.750000 | 461 | 1960-10-01 |

| 142 | 1960.833333 | 390 | 1960-11-01 |

| 143 | 1960.916667 | 432 | 1960-12-01 |

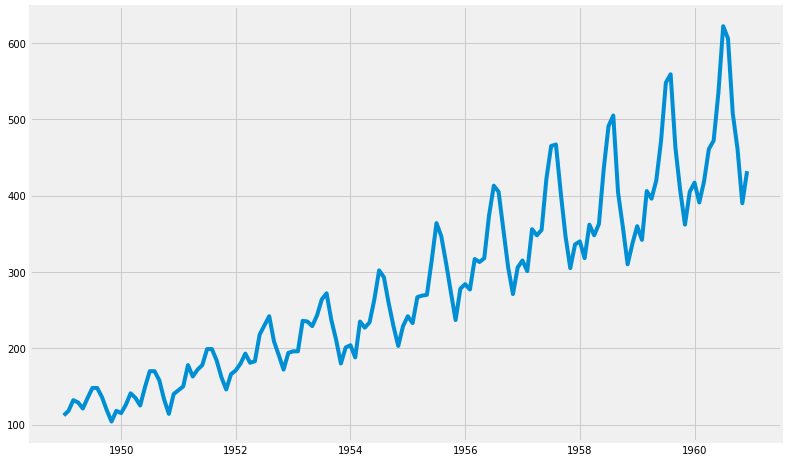

4) 시각화

(1) 그래프

t = df.time

y = df.AirPassengers

plt.figure(figsize=(12, 8))

plt.plot(t, y)

plt.show()

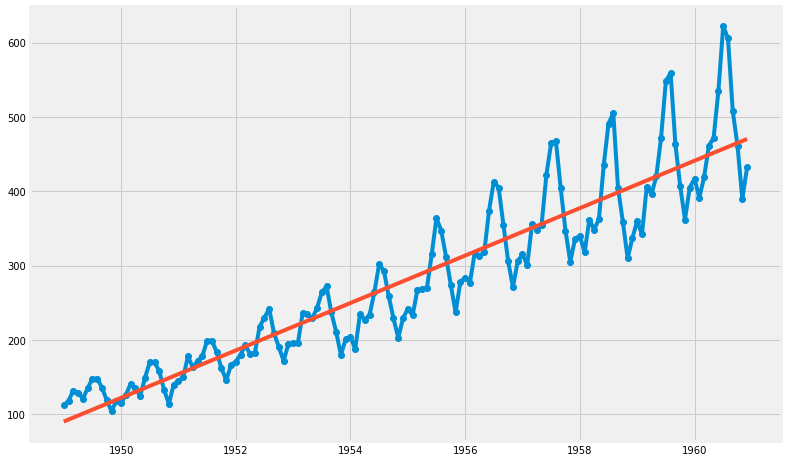

(2) 직선 추가

- OLS : Ordinary Least Square 함수

- AirPassengers ~ time 관계로부터, ➜ AirPassengers = param1 + param2 * time

result = sm.OLS.from_formula( "AirPassengers ~ time", data=df ).fit()

print( result.params )

print( result.params[0], result.params[1] )

Intercept -62055.907280

time 31.886207

dtype: float64

-62055.9072797 31.8862068965

t = df.time

y = df.AirPassengers

trend = result.params[0] + result.params[1] * t

plt.figure(figsize=(12, 8))

plt.plot(t, y, 'o-', t, trend, '-')

plt.show()

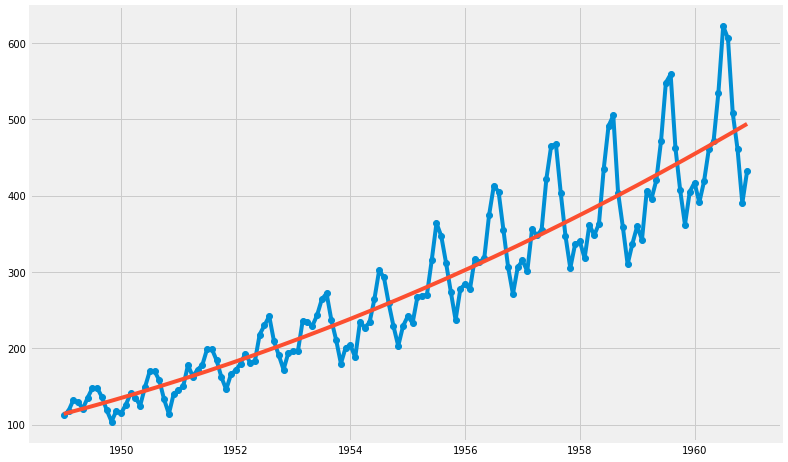

(3) 2차 함수

- AirPassengers ~ time + np.power(time, 2)

- ➜ AirPassengers = time + time^2

result2 = sm.OLS.from_formula( "AirPassengers ~ time + np.power(time, 2)", data=df ).fit()

print( result2.params[0], result2.params[1], result2.params[2] )

3794880.89376 -3913.9256755 1.00918055774

trend2 = result2.params[0] + result2.params[1] * t + result2.params[2]* t**2

plt.figure(figsize=(12, 8))

plt.plot(t, y, 'o-', t, trend2, '-')

plt.show()

3. statsmodels - 시계열 데이터(Time Series)

1) 시계열 데이터

- 시계열 데이터는 대부분 예측에 활용된다.

- 여기에서는 예측 모델로서 ARIMA 모형을 채택하였다. (Auto Regressive Integrated Moving Average)

- 과거의 관측값과 오차를 사용해서 현재의 시계열 값을 설명하는 ARMA 모델을 일반화 한 것입니다. 이는 ARMA 모델이 안정적 시계열(Stationary Series)에만 적용 가능한 것에 비해, 분석 대상이 약간은 비안정적 시계열(Non Stationary Series)의 특징을 보여도 적용이 가능하다는 의미입니다.

(1) 안정적 시계열 (Stationary Series)

- 평균 불변 (시간에 따라 변하지만 그 평균은 불변)

- 분산 불변

- 공분산 불변

- 간단히 말하면, 모든 t(시간)에 대하여 통계치 p(x)가 동일함

(2) 비안정적 시계열(Non Stationary Series)의 처리

- 차분, 로그 등을 활용하여 안정적 시계열로 변환한 후 ARIMA 모형 적용함

(3) ARIMA 모형 ( Box-Jenkins approach ) 적용

자기회귀이동평균(ARMA) 모형 - 매우 좋다 !!!

1단계. 시계열 자료를 시각화 해서 안정적 시계열인지를 확인한다. Visualize the time series

2단계. 시계열 자료를 안정적 시계열로 변환한다. Stationarize the series

3단계. ACF/PACF차트나 auto.arima 함수를 사용하여 최적화된 파라미터를 찾는다. Plot ACF/PACF charts and find optimal parameters

4단계. ARIMA 모형을 만든다. Build the ARIMA model

5단계. (필요한 경우) 미래 추이에 대해 예측한다. Make prediction

2) 대상 데이터 얻기

%matplotlib inline

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import datetime

from dateutil.relativedelta import relativedelta

import seaborn as sns

import statsmodels.api as sm

from statsmodels.tsa.stattools import acf

from statsmodels.tsa.stattools import pacf

from statsmodels.tsa.seasonal import seasonal_decompose

df = pd.read_csv( './data_science/07. portland-oregon-average-monthly-.csv', index_col=0 )

df.index.name=None

df.reset_index(inplace=True)

df.head(3)

| index | Portland Oregon average monthly bus ridership (/100) January 1973 through June 1982, n=114 | |

|---|---|---|

| 0 | 1960-01 | 648 |

| 1 | 1960-02 | 646 |

| 2 | 1960-03 | 639 |

start = datetime.datetime.strptime("1973-01-01", "%Y-%m-%d")

date_list = [start + relativedelta(months=x) for x in range(0, len(df)) ]

df['index'] = date_list

df.set_index( ['index'], inplace=True)

df.index.name=None

df.head(3)

| Portland Oregon average monthly bus ridership (/100) January 1973 through June 1982, n=114 | |

|---|---|

| 1973-01-01 | 648 |

| 1973-02-01 | 646 |

| 1973-03-01 | 639 |

df.columns = ['riders']

df['riders'] = df.riders.apply( lambda x: int(x)*100 )

df.head()

| riders | |

|---|---|

| 1973-01-01 | 64800 |

| 1973-02-01 | 64600 |

| 1973-03-01 | 63900 |

| 1973-04-01 | 65400 |

| 1973-05-01 | 63000 |

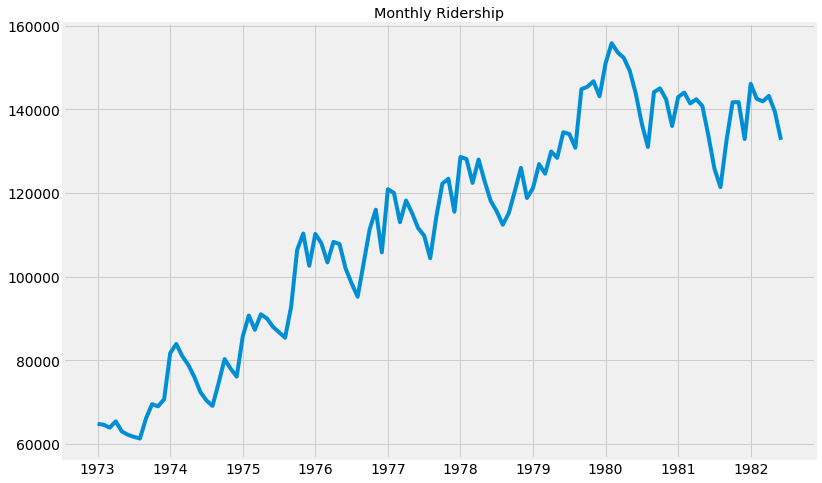

3) 시각화 (Visualization)

- 안정적 시계열이 아니다 !!!

df.riders.plot(

figsize=(12, 8),

title='Monthly Ridership',

fontsize=14

)

plt.savefig(

'month_ridership.png',

bbox_inches='tight'

)

4) 안정화 및 적용할 통계 모형 찾기

(1) 시계열 데이터의 요소 및 분해

- 시계열 데이터 = 패턴 + 랜덤

- 패턴 = 트랜드 패턴 + 주기 패턴 + seasonal 패턴 + 기타 통계적 패턴

- 시계열 데이터에서 패턴을 제거한 나머지(잔차)에 대해 ARIMA(p, q) 모형을 적용하여 p, q를 구하면 대략적으로 적용할 모델을 찾을 수 있다.

- 이를 통하여 예측할 수 있다.

(2) 모형 적용

- 랜덤 요소 : ARIMA, ARCH 등 적용

- 패턴 - 트랜드 : 다양한 통계 모형 적용

- 패턴 - Seasonal, 주기 : ACF, Fourier 방법

- 패턴 - 기타 통계적 방법 : 데이터 마이닝 기법 (의사결정나무, SVM 등)

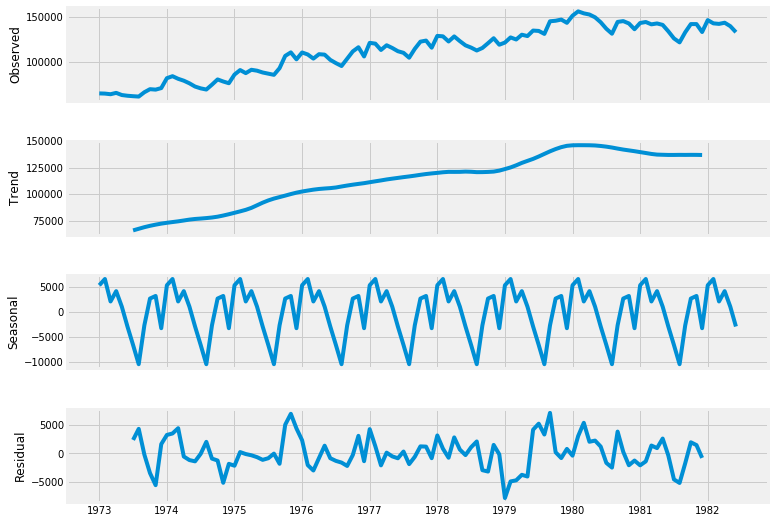

decomposition = seasonal_decompose( df.riders, freq=12 )

fig = plt.figure()

fig = decomposition.plot()

fig.set_size_inches(12, 8)

<matplotlib.figure.Figure at 0x7f3e45cc85f8>

trend = decomposition.trend

seasonal = decomposition.seasonal

residual = decomposition.resid

(3) 그리드 서치 p, q

# Define the p, d and q parameters to take any value between 0 and 2

p = d = q = range(0, 2)

# Generate all different combinations of p, q and d triplets

pdq = list( itertools.product(p, d, q))

# Generate all different combinations of seasonal p, q and d triplets

seasonal_pdq = [ (x[0], x[1], x[2], 12) for x in pdq ]

print('Example of parameter combinations for Seasonal ARIMA ...')

print('SARIMAX: {} x {}'.format(pdq[1], seasonal_pdq[1]) )

print('SARIMAX: {} x {}'.format(pdq[1], seasonal_pdq[2]) )

print('SARIMAX: {} x {}'.format(pdq[2], seasonal_pdq[3]) )

print('SARIMAX: {} x {}'.format(pdq[2], seasonal_pdq[4]) )

Example of parameter combinations for Seasonal ARIMA ...

SARIMAX: (0, 0, 1) x (0, 0, 1, 12)

SARIMAX: (0, 0, 1) x (0, 1, 0, 12)

SARIMAX: (0, 1, 0) x (0, 1, 1, 12)

SARIMAX: (0, 1, 0) x (1, 0, 0, 12)

warnings.filterwarnings("ignore")

select_candi = 10000000

param_candi = ( 0, 0, 0 )

param_seasonal_candi = ( 0, 0, 0)

count=0

end_count = len(pdq)

for param in pdq:

for param_seasonal in seasonal_pdq:

try:

mod = sm.tsa.statespace.SARIMAX( df['riders'],

order=param,

seasonal_order=param_seasonal,

enforce_stationarity=False,

enforce_invertibility=False

)

results = mod.fit()

count += 1

if count <= 5:

print('ARIMA{}x{}12 - AIC:{}'.format(param, param_seasonal, results.aic))

if results.aic < select_candi:

select_candi = results.aic

param_candi = param

param_seasonal_candi = param_seasonal

except:

continue

print(param_candi, param_seasonal_candi, select_candi)

ARIMA(0, 0, 0)x(0, 0, 1, 12)12 - AIC:2595.3864799134485

ARIMA(0, 0, 0)x(0, 1, 1, 12)12 - AIC:1948.42720635445

ARIMA(0, 0, 0)x(1, 0, 0, 12)12 - AIC:2200.3535348493824

ARIMA(0, 0, 0)x(1, 0, 1, 12)12 - AIC:2178.6806032356317

ARIMA(0, 0, 0)x(1, 1, 0, 12)12 - AIC:1962.501941516448

(0, 1, 1) (0, 1, 1, 12) 1688.69970004

mod = sm.tsa.statespace.SARIMAX(

df['riders'],

order=(0, 1, 1),

seasonal_order=(0, 1, 1, 12),

enforce_stationarity=False,

enforce_invertibility=False

)

results = mod.fit()

print( results.summary().tables[1] )

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ma.L1 0.0244 0.099 0.246 0.806 -0.170 0.219

ma.S.L12 -0.3808 0.072 -5.256 0.000 -0.523 -0.239

sigma2 1.519e+07 2.14e+06 7.089 0.000 1.1e+07 1.94e+07

==============================================================================

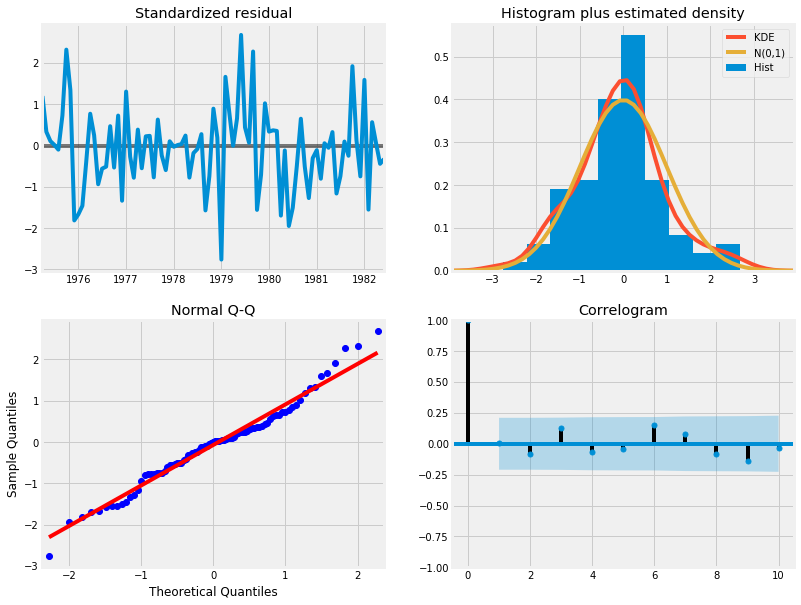

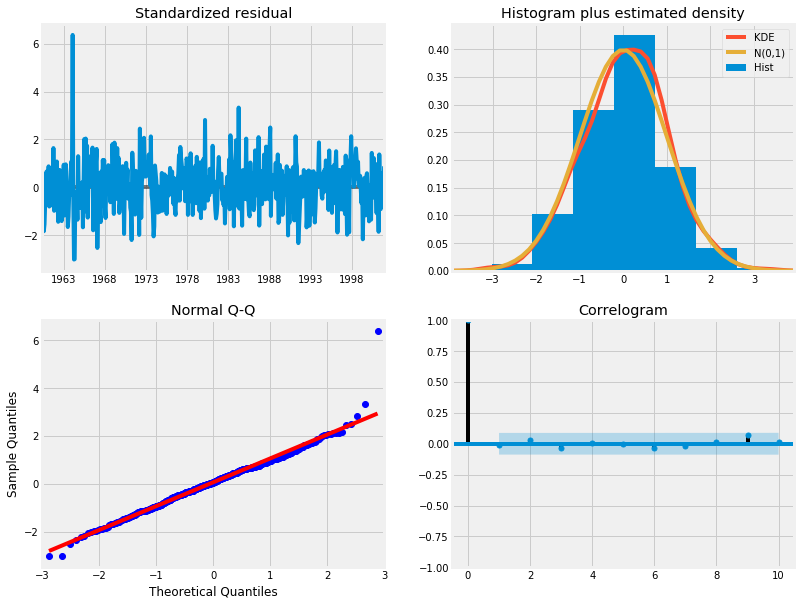

results.plot_diagnostics( figsize=(12, 10) )

plt.show()

(4) 분석

- Histogram plus estimated density에서 KDE, N(0,1)이 정규분포를 따르는 것으로 보인다.

- Normal Q-Q 에서 선형성이 두드러진다.

- Standardized residual에서 어떤 경향성도 보이지 않아 White Noise로 보인다.

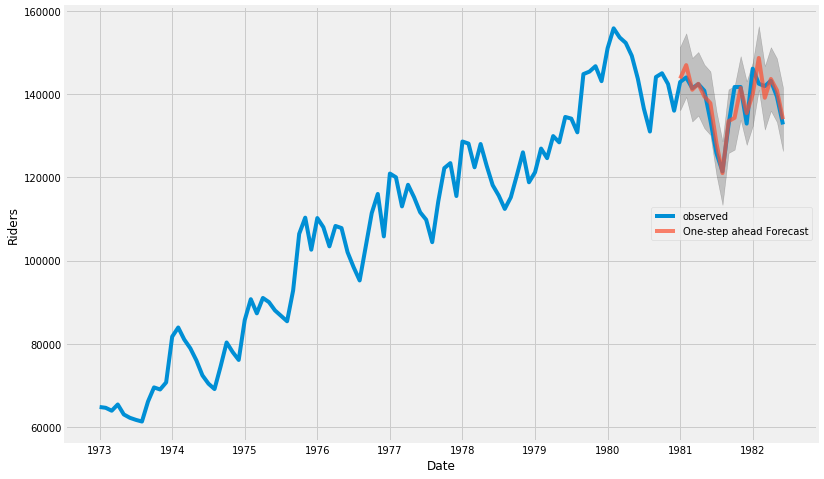

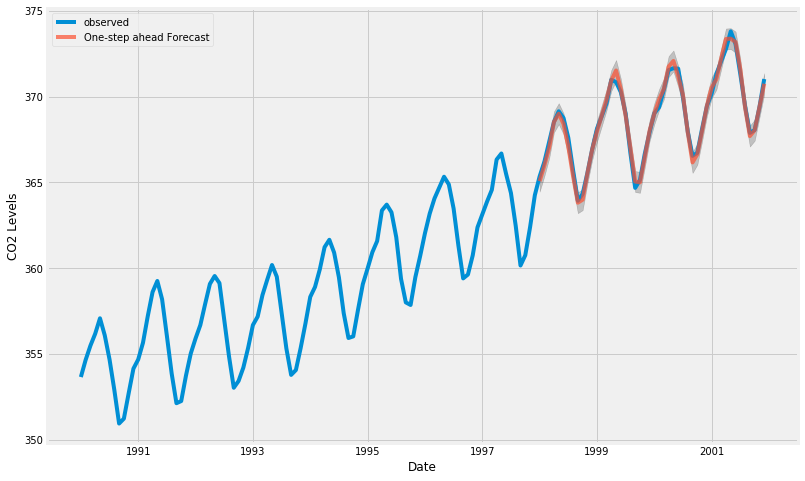

(5) 예측 관찰

- 원 데이터의 시계열이 73년부터 82년 중반까지이다.

- 예측을 1981. 1. 1.부터 한다면, 73년부터 1980.12.31.까지의 데이터를 바탕으로 한 예측에 대해 원 데이터의 1981.1.1.부터 82년 중반까지의 데이터와 비교해 볼 수 있다.

pred = results.get_prediction(

start=pd.to_datetime('1981-01-01'),

dynamic=False

)

pred_ci = pred.conf_int()

# 관측 데이터 1973년 부터 끝까지

ax = df['riders']['1973' : ].plot( label='observed', figsize=(12, 8) )

# 예측

pred.predicted_mean.plot(

ax=ax,

label='One-step ahead Forecast',

alpha=.7

)

ax.fill_between(

pred_ci.index,

pred_ci['lower riders'],

pred_ci['upper riders'],

color='k',

alpha=.2

)

ax.set_xlabel('Date')

ax.set_ylabel('Riders')

plt.legend(loc=5)

plt.show()

y_forecasted = pred.predicted_mean

y_truth = df['riders']['1981-01-01' : ]

# Compute the Mean Square Error

mse = (( y_forecasted - y_truth ) ** 2).mean()

print('The Mean Squared Error of our forecasts is {}'.format( round(mse, 2) ) )

The Mean Squared Error of our forecasts is 10215528.27

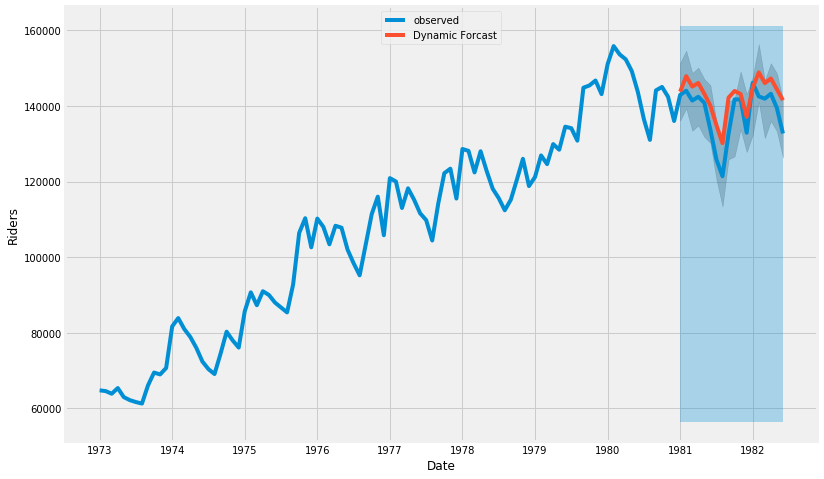

pred_dynamic = results.get_prediction(

start=pd.to_datetime('1981-01-01'),

dynamic=True,

full_results=True

)

pred_dynamic_ci = pred_dynamic.conf_int()

# 관측 데이터 1973년 부터 끝까지

ax = df['riders']['1973' : ].plot( label='observed', figsize=(12, 8) )

# 예측

pred_dynamic.predicted_mean.plot(

ax=ax,

label='Dynamic Forcast'

)

ax.fill_between(

pred_ci.index,

pred_ci['lower riders'],

pred_ci['upper riders'],

color='k',

alpha=.2

)

ax.fill_betweenx(

ax.get_ylim(),

pd.to_datetime('1981-01-01'),

df.index[-1],

alpha=.3

)

ax.set_xlabel('Date')

ax.set_ylabel('Riders')

plt.legend(loc=9)

plt.show()

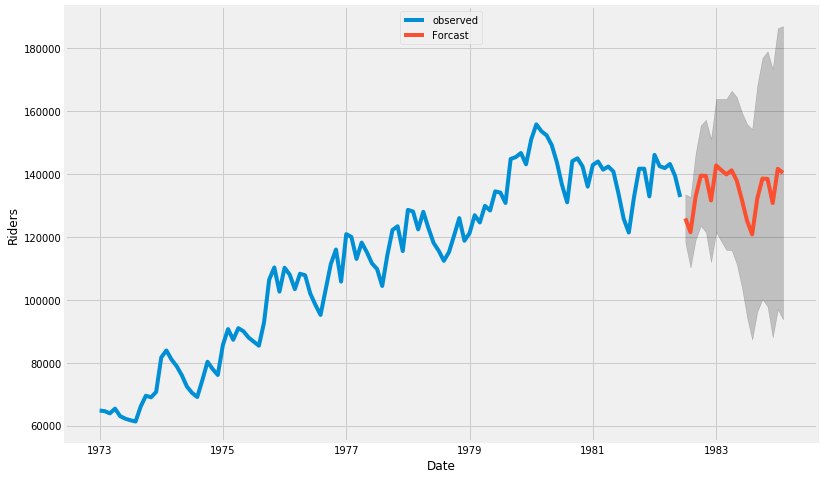

(6) 예측

- 관측 데이터(~82년 중반까지)를 넘어서서 그 이후의 모습을 예측하는 그래프를 그린다.

# Extract the predicted and true values of our time series

y_forecasted = pred_dynamic.predicted_mean

y_truth = df['riders']['1981-01-01' : ]

# Compute the Mean Square Error

mse = (( y_forecasted - y_truth ) ** 2).mean()

print('The Mean Squared Error of our forecasts is {}'.format( round(mse, 2) ) )

The Mean Squared Error of our forecasts is 30029929.6

# Get forecast some steps ahead in future

pred_uc = results.get_forecast( steps=20 )

# Get confidence intervals of forecasts

pred_ci = pred_uc.conf_int()

# 관측 데이터 1973년 부터 끝까지

ax = df['riders']['1973' : ].plot( label='observed', figsize=(12, 8) )

# 예측

pred_uc.predicted_mean.plot(

ax=ax,

label='Forcast'

)

ax.fill_between(

pred_ci.index,

pred_ci['lower riders'],

pred_ci['upper riders'],

color='k',

alpha=.2

)

ax.set_xlabel('Date')

ax.set_ylabel('Riders')

plt.legend(loc=9)

plt.show()

3. statsmodels : 예제2- 하와이 대기 CO2비중

- Atmospheric CO2 from Continous Air Samples at Mauna Loa Observatory, Hawaii, U.S.A.

1) 데이터 얻기

data = sm.datasets.co2.load_pandas()

y = data.data

y.head()

| co2 | |

|---|---|

| 1958-03-29 | 316.1 |

| 1958-04-05 | 317.3 |

| 1958-04-12 | 317.6 |

| 1958-04-19 | 317.5 |

| 1958-04-26 | 316.4 |

y = y['co2'].resample('MS').mean()

y = y.fillna(y.bfill())

y.head()

1958-03-01 316.100000

1958-04-01 317.200000

1958-05-01 317.433333

1958-06-01 315.625000

1958-07-01 315.625000

Freq: MS, Name: co2, dtype: float64

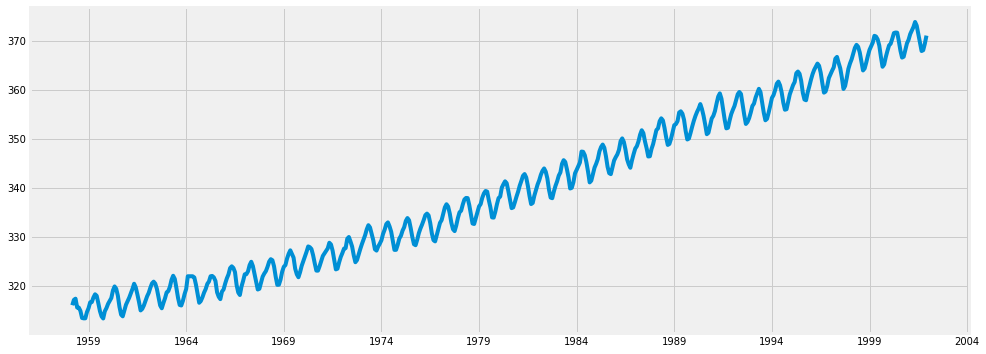

2) 기본 그래프

y.plot( figsize=(15, 6) )

plt.show()

3) 그리드 서치

# Define the p, d and q parameters to take any value between 0 and 2

p = d = q = range(0, 2)

# Generate all different combinations of p, q and d triplets

pdq = list( itertools.product(p, d, q))

# Generate all different combinations of seasonal p, q and d triplets

seasonal_pdq = [ (x[0], x[1], x[2], 12) for x in pdq ]

print('Example of parameter combinations for Seasonal ARIMA ...')

print('SARIMAX: {} x {}'.format(pdq[1], seasonal_pdq[1]) )

print('SARIMAX: {} x {}'.format(pdq[1], seasonal_pdq[2]) )

print('SARIMAX: {} x {}'.format(pdq[2], seasonal_pdq[3]) )

print('SARIMAX: {} x {}'.format(pdq[2], seasonal_pdq[4]) )

Example of parameter combinations for Seasonal ARIMA ...

SARIMAX: (0, 0, 1) x (0, 0, 1, 12)

SARIMAX: (0, 0, 1) x (0, 1, 0, 12)

SARIMAX: (0, 1, 0) x (0, 1, 1, 12)

SARIMAX: (0, 1, 0) x (1, 0, 0, 12)

warnings.filterwarnings("ignore")

select_candi = 10000000

param_candi = ( 0, 0, 0 )

param_seasonal_candi = ( 0, 0, 0)

count=0

end_count = len(pdq)

for param in pdq:

for param_seasonal in seasonal_pdq:

try:

mod = sm.tsa.statespace.SARIMAX(

# 여기 !!!

y,

order=param,

seasonal_order=param_seasonal,

enforce_stationarity=False,

enforce_invertibility=False

)

results = mod.fit()

count += 1

if count <= 5:

print('ARIMA{}x{}12 - AIC:{}'.format(param, param_seasonal, results.aic))

if results.aic < select_candi:

select_candi = results.aic

param_candi = param

param_seasonal_candi = param_seasonal

except:

continue

print(param_candi, param_seasonal_candi, select_candi)

ARIMA(0, 0, 0)x(0, 0, 1, 12)12 - AIC:6787.343624040217

ARIMA(0, 0, 0)x(0, 1, 1, 12)12 - AIC:1596.711172764377

ARIMA(0, 0, 0)x(1, 0, 0, 12)12 - AIC:1058.9388921320035

ARIMA(0, 0, 0)x(1, 0, 1, 12)12 - AIC:1056.2878485614463

ARIMA(0, 0, 0)x(1, 1, 0, 12)12 - AIC:1361.6578978073326

(1, 1, 1) (1, 1, 1, 12) 277.780217493

mod = sm.tsa.statespace.SARIMAX(

y,

order=(1, 1, 1),

seasonal_order=(1, 1, 1, 12),

enforce_stationarity=False,

enforce_invertibility=False

)

results = mod.fit()

print( results.summary().tables[1] )

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.3182 0.092 3.442 0.001 0.137 0.499

ma.L1 -0.6254 0.077 -8.164 0.000 -0.776 -0.475

ar.S.L12 0.0010 0.001 1.732 0.083 -0.000 0.002

ma.S.L12 -0.8769 0.026 -33.811 0.000 -0.928 -0.826

sigma2 0.0972 0.004 22.632 0.000 0.089 0.106

==============================================================================

results.plot_diagnostics( figsize=(12, 10) )

plt.show()

pred = results.get_prediction(

start=pd.to_datetime('1998-01-01'),

dynamic=False

)

pred_ci = pred.conf_int()

# 관측 데이터 1973년 부터 끝까지

ax = y[ '1990' : ].plot( label='observed', figsize=(12, 8) )

# 예측

pred.predicted_mean.plot(

ax=ax,

label='One-step ahead Forecast',

alpha=.7

)

ax.fill_between(

pred_ci.index,

pred_ci.iloc[ : , 0 ],

pred_ci.iloc[ : , 1 ],

color='k',

alpha=.2

)

ax.set_xlabel('Date')

ax.set_ylabel('CO2 Levels')

plt.legend()

plt.show()

y_forecasted = pred.predicted_mean

y_truth = y['1998-01-01' : ]

# Compute the Mean Square Error

mse = (( y_forecasted - y_truth ) ** 2).mean()

print('The Mean Squared Error of our forecasts is {}'.format( round(mse, 2) ) )

The Mean Squared Error of our forecasts is 0.07

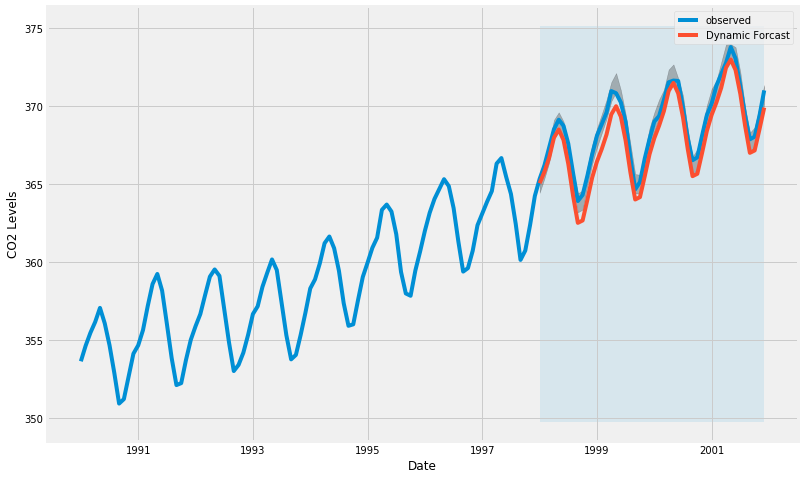

pred_dynamic = results.get_prediction(

start=pd.to_datetime('1998-01-01'),

dynamic=True,

full_results=True

)

pred_dynamic_ci = pred_dynamic.conf_int()

# 관측 데이터 1973년 부터 끝까지

ax = y['1990' : ].plot( label='observed', figsize=(12, 8) )

# 예측

pred_dynamic.predicted_mean.plot(

ax=ax,

label='Dynamic Forcast'

)

ax.fill_between(

pred_ci.index,

pred_ci.iloc[ : , 0 ],

pred_ci.iloc[ : , 1 ],

color='k',

alpha=.25

)

ax.fill_betweenx(

ax.get_ylim(),

pd.to_datetime('1998-01-01'),

y.index[-1],

alpha=.1,

zorder=-1

)

ax.set_xlabel('Date')

ax.set_ylabel('CO2 Levels')

plt.legend()

plt.show()

# Extract the predicted and true values of our time series

y_forecasted = pred_dynamic.predicted_mean

y_truth = y['1998-01-01' : ]

# Compute the Mean Square Error

mse = (( y_forecasted - y_truth ) ** 2).mean()

print('The Mean Squared Error of our forecasts is {}'.format( round(mse, 2) ) )

The Mean Squared Error of our forecasts is 1.01

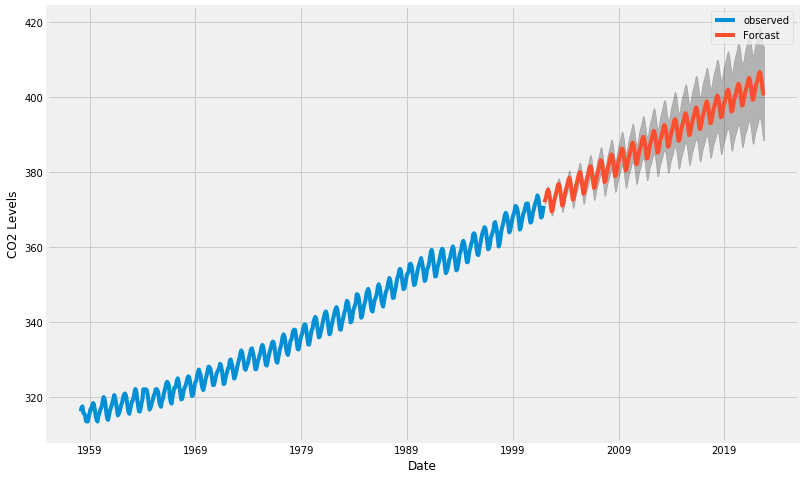

# Get forecast some steps ahead in future

pred_uc = results.get_forecast( steps=250 )

# Get confidence intervals of forecasts

pred_ci = pred_uc.conf_int()

# 관측 데이터 1973년 부터 끝까지

ax = y.plot( label='observed', figsize=(12, 8) )

# 예측

pred_uc.predicted_mean.plot(

ax=ax,

label='Forcast'

)

ax.fill_between(

pred_ci.index,

pred_ci.iloc[ : , 0 ],

pred_ci.iloc[ : , 1 ],

color='k',

alpha=.25

)

ax.set_xlabel('Date')

ax.set_ylabel('CO2 Levels')

plt.legend()

plt.show()